What is the Work Allowance for Universal Credit?

If you’re working and claiming Universal Credit, it’s important to understand how your earnings affect your monthly payments. The work allowance is the amount you can earn before your Universal Credit starts to reduce.

It’s designed to support those who are in work while still receiving financial help. The amount of work allowance you get depends on whether your Universal Credit includes housing support.

For the 2025/26 tax year, this figure has been updated, giving claimants more clarity. Understanding the work allowance helps you plan your income and ensures you’re not caught off guard by payment deductions.

How Does the Work Allowance Affect Your Universal Credit Payments?

The work allowance sets the earnings threshold before any deductions are made to your Universal Credit. If your income stays below this threshold, you receive your full Universal Credit entitlement.

Once your earnings go over this amount, your payment is reduced. This deduction occurs through a taper rate, which currently stands at 55 pence for every £1 earned above the allowance.

For example, if your allowance is £684 and you earn £784, only £100 is considered for deduction, resulting in a £55 reduction. This system ensures you’re always better off working, while gradually reducing support as earnings rise.

What Are the Work Allowance Amounts for the 2025/26 Tax Year?

In the 2025/26 tax year, the work allowance depends on whether you receive housing support through Universal Credit. If your Universal Credit includes help with housing costs, the lower work allowance applies. Without housing support, the allowance is higher.

These thresholds help the government balance financial support and encourage employment. The updated amounts for the tax year are as follows:

| Type of Universal Credit Claim | Monthly Work Allowance (2025/26) |

| With housing support | £411 |

| Without housing support | £684 |

These figures represent the limit you can earn before deductions begin through the taper rate.

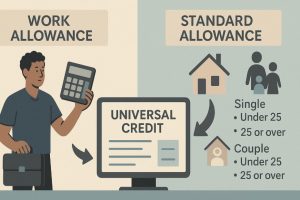

What’s the Difference Between Work Allowance and Standard Allowance?

The work allowance and standard allowance are distinct components of Universal Credit. The standard allowance is the baseline monthly amount provided depending on your age and whether you’re in a couple or single.

The work allowance, on the other hand, is the amount you can earn before your benefit starts to reduce. These two values serve different purposes and should not be confused.

The standard allowance is fixed based on circumstances, while the work allowance relates to earnings. The table below shows the key differences:

| Feature | Standard Allowance | Work Allowance |

| Based on | Personal and household status | Employment and housing status |

| Amount (example only) | Varies by age and household | £411 or £684, depending on housing cost |

| Impact on payments | Initial base payment amount | Affects how much of UC is reduced |

Understanding both helps you estimate your total UC entitlement.

When Do You Qualify for the Work Allowance in Universal Credit?

Not everyone on Universal Credit qualifies for the work allowance. It’s specifically available to people who are working and either have children or are assessed as having limited capability for work.

If you’re in either of these groups, you’re eligible to earn up to the work allowance before your benefits start to decrease. However, if you don’t meet these criteria, your earnings reduce your Universal Credit from the first pound.

You qualify for the work allowance if you meet the following:

- You’re responsible for a child or a qualifying young person.

- You’ve been assessed as having limited capability for work.

- You are in paid employment (including self-employment).

- Your Universal Credit payment includes a work component.

If none of the above apply, then your Universal Credit will start to reduce immediately when you earn, using the taper rate. Always check your UC journal or contact your work coach to clarify your eligibility.

What is the Universal Credit Taper Rate and How Does It Work?

The taper rate is the percentage of your earnings that is deducted from your Universal Credit payment once you exceed your work allowance. It’s a gradual way to reduce financial support as you earn more, encouraging work while providing a safety net.

As of the 2025/26 tax year, the taper rate is set at 55 percent. This means for every pound earned above your allowance, your Universal Credit is reduced by 55p.

If your earnings increase significantly, your Universal Credit can be reduced to zero, but not instantly, it’s tapered off over time to prevent sudden income loss.

How Does the Housing Element Impact Your Work Allowance?

The inclusion of a housing element in your Universal Credit claim lowers your work allowance. This is because the government already supports your housing needs through the UC housing component.

Why Does Housing Support Reduce the Work Allowance?

When your Universal Credit includes a housing element, your work allowance is reduced to ensure balanced support across different claim types. The idea is that those receiving help with rent or mortgage need slightly less in work allowance to equalise overall assistance.

Here’s how the difference is applied:

- With housing support:

- You receive a lower work allowance (£411).

- The system balances housing and income support.

- Without housing support:

- You receive a higher work allowance (£684).

- This offsets the lack of rental support.

This system aims to provide fair benefits based on total need rather than just income.

Is There a Higher Allowance Without Housing Costs?

Yes, claimants without any housing support in their Universal Credit receive a higher work allowance. This is currently set at £684 per month for the 2025/26 tax year.

This higher threshold helps balance the absence of housing support. If you cover your rent or mortgage independently, this higher allowance ensures you’re not penalised when working.

It provides an extra cushion before deductions begin, helping make work more financially beneficial even without rental help.

Can You Increase Your Universal Credit by Adjusting Your Income?

Yes, managing your income wisely can optimise your Universal Credit payments. If you’re self-employed or have fluctuating earnings, it may be possible to time your income to stay below or close to the work allowance.

While deliberate income manipulation isn’t encouraged, being aware of how your pay periods affect UC calculations can help. You can also adjust work hours, track expenses carefully, and plan for deductions.

For some, taking on irregular shifts in specific months might make a significant difference. Understanding how your income interacts with the allowance and taper rate gives you more control over your payments.

How Do Earnings Over the Threshold Reduce Your Benefit?

Once you exceed your work allowance, your Universal Credit payment begins to reduce through the taper rate. This system ensures that work still pays but gradually lessens financial support. The reduction is calculated as 55 pence for every pound earned over the work allowance.

Here’s how it affects your benefit:

- You earn above your allowance.

- The excess is calculated (e.g. £100 over).

- Multiply the excess by 0.55.

- The resulting amount is deducted from your UC.

This taper system ensures a smooth transition from benefits to financial independence.

What Happens If You Earn Just Above the Allowance?

Even if your earnings slightly exceed your allowance, the deduction is proportional, not immediate or drastic. Let’s break it down:

- Example: Your allowance is £684, and you earn £700.

- The excess is £16.

- 55 percent of £16 = £8.80 reduction.

Key points to remember:

- You still receive most of your UC.

- Earnings just over the limit only trigger small deductions.

- There’s no sudden cut-off or loss of benefit.

This ensures every pound you earn still leads to more overall income.

How Is the 55p Deduction Calculated?

The deduction uses a simple formula. First, your monthly income is compared against your work allowance. Any amount above the allowance is multiplied by 0.55.

For example, if you earn £200 over your allowance, your Universal Credit will be reduced by £110. This calculation happens automatically and is updated monthly in your UC statement.

It helps maintain a balance between earned income and ongoing support, making the transition to full employment smoother.

Where Can You Find the Official Guidance on Work Allowance?

You can always find the latest information on work allowance and how it affects your Universal Credit through official government websites and tools.

These sources explain the current thresholds, eligibility, and taper rates in detail. You can also use online calculators to estimate how your earnings will impact your UC payments.

Keeping up with this guidance ensures you’re aware of any updates that might change your entitlements in future tax years. It’s recommended to regularly check your UC journal and government advice platforms for personalised information relevant to your claim.

Conclusion

Understanding the work allowance for Universal Credit is crucial if you’re employed and receiving support. It sets the limit on how much you can earn before your benefit is reduced and helps maintain a balance between working and claiming.

Whether you qualify for the higher or lower allowance depends on your circumstances, especially housing. With the updated figures for 2025/26, it’s more important than ever to check your income against the allowance and track changes in your UC statement.

By staying informed, you can better manage your finances and make the most of the support available.

FAQs About Work Allowance

How often is the work allowance amount updated in the UK?

The work allowance is typically reviewed annually in line with the UK tax year, which begins every April. Adjustments are influenced by economic conditions and government welfare policy changes.

Does having children affect your work allowance eligibility?

Yes, if you’re responsible for a child or have limited capability for work, you may qualify for the work allowance. Without these, you won’t receive the work allowance.

Can both members of a couple receive a work allowance?

No, only one work allowance is applied per Universal Credit claim, even if both partners are working. The system calculates it based on the couple’s combined earnings.

What counts as earnings under Universal Credit?

Earnings include wages from employment or self-employment, bonuses, and other taxable income. Some deductions like tax and National Insurance may be excluded from this total.

Are self-employed people treated differently for work allowance?

Self-employed claimants still get a work allowance, but their income is assessed using the Minimum Income Floor (MIF), which may affect how much UC they receive.

How do changes in income affect monthly UC calculations?

Universal Credit is adjusted monthly. If your income increases above the work allowance, your UC payment may decrease in that assessment period due to the taper rate.

Can part-time workers still benefit from the work allowance?

Absolutely. Part-time workers can still qualify for the work allowance, and it helps reduce how much their UC is reduced as their earnings increase.

Read Next:

How Much Universal Credit Will I Get if I Earn £600 a Month in the UK?

How Much Universal Credit Will I Get If I Earn £1,000 a Month?

How Much Universal Credit Will I Get If I Earn £1,200 a Month? | Calculating UC Benefits

How Much Universal Credit Will I Get if I Earn 1500 a Month?

How Much Universal Credit Will I Get If I Earn £2,000 a Month?