How Much Can You Earn and Still Get Universal Credit? | Maximum Limits

Universal Credit is a flexible benefits system introduced in the UK to simplify welfare payments and support people as they transition into work or manage their finances while working.

However, understanding how much you can earn while still qualifying for Universal Credit can be complex, with various factors like housing costs, childcare, and disabilities affecting the amount you receive.

This detailed guide will help you understand the income thresholds, work allowances, and taper rates, along with examples to make calculating your entitlements easier.

Whether you’re working part-time, full-time, or managing multiple jobs, knowing these details can help you optimise your finances.

What are the Universal Credit Earnings Thresholds?

Universal Credit payments are based on your earnings, living situation, and household composition. The standard amount is the foundation of your Universal Credit calculation.

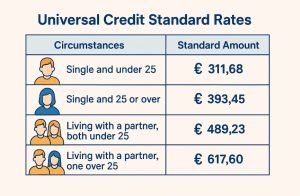

Standard Monthly Amounts:

These are the baseline amounts you can expect to receive, depending on your age and relationship status:

| Circumstances | Standard Amount (Monthly) |

| Single and under 25 | £311.68 |

| Single and 25 or over | £393.45 |

| Living with a partner, both under 25 | £489.23 |

| Living with a partner, one over 25 | £617.60 |

You may receive additional elements if you:

- Pay for housing or rent.

- Have children or childcare costs.

- Are unable to work due to sickness or disability.

- Care for someone with a disability.

What Is the Work Allowance?

The work allowance is the amount you can earn before Universal Credit payments are reduced. Your allowance depends on whether you claim the housing element as part of your Universal Credit.

| Situation | Monthly Work Allowance |

|---|---|

| With housing element | £404.00 |

| Without housing element | £673.00 |

Once you exceed your work allowance, your Universal Credit is reduced by 55p for every £1 earned over the threshold, this is known as the taper rate.

Tip: If you’re eligible for the work allowance, your Universal Credit goes further — especially important for parents or disabled individuals.

How Much Universal Credit Will I Get Based on Monthly Earnings?

Let’s break down the Universal Credit you may receive for different earning levels, assuming you are entitled to the housing element and have a work allowance of £404/month.

How Much Universal Credit Will I Get if I Earn £600 a Month?

Scenario:

- Earnings: £600/month

- Work Allowance: £404/month

- Excess Earnings: £600 – £404 = £196

The taper rate of 55% is applied to excess earnings:

- Reduction = £196 × 0.55 = £107.80

If your standard Universal Credit entitlement (including housing or other elements) is £1,400, your reduced payment will be:

- £1,400 – £107.80 = £1,292.20

How Much Universal Credit Will I Get if I Earn £1,000 a Month?

Scenario:

- Earnings: £1,000/month

- Work Allowance: £404/month

- Excess Earnings: £1,000 – £404 = £596

The taper rate of 55% is applied to excess earnings:

- Reduction = £596 × 0.55 = £327.80

If your standard Universal Credit entitlement is £1,400, your reduced payment will be:

- £1,400 – £327.80 = £1,072.20

How Much Universal Credit Will I Get if I Earn £1,200 a Month?

Scenario:

- Earnings: £1,200/month

- Work Allowance: £404/month

- Excess Earnings: £1,200 – £404 = £796

The taper rate of 55% is applied to excess earnings:

- Reduction = £796 × 0.55 = £437.80

If your standard Universal Credit entitlement is £1,400, your reduced payment will be:

- £1,400 – £437.80 = £962.20

How Much Universal Credit Will I Get if I Earn £1,500 a Month?

Scenario:

- Earnings: £1,500/month

- Work Allowance: £404/month

- Excess Earnings: £1,500 – £404 = £1,096

The taper rate of 55% is applied to excess earnings:

- Reduction = £1,096 × 0.55 = £602.80

If your standard Universal Credit entitlement is £1,400, your reduced payment will be:

- £1,400 – £602.80 = £797.20

How Much Universal Credit Will I Get if I Earn £2,000 a Month?

Scenario:

- Earnings: £2,000/month

- Work Allowance: £404/month

- Excess Earnings: £2,000 – £404 = £1,596

The taper rate of 55% is applied to excess earnings:

- Reduction = £1,596 × 0.55 = £877.80

If your standard Universal Credit entitlement is £1,400, your reduced payment will be:

- £1,400 – £877.80 = £522.20

Key Insights

- If your income rises significantly (e.g., beyond £2,000/month), your Universal Credit could reduce to a point where it no longer applies.

- The amount you receive depends heavily on your standard amount, work allowance, and any additional elements such as housing or childcare.

Earnings and Your Responsibilities: What You Need to Know?

When you claim Universal Credit, you enter into an agreement with the Department for Work and Pensions (DWP) regarding what is expected of you to maintain your eligibility. These responsibilities vary based on your earnings and are outlined in your claimant commitment. This document sets out your obligations to:

- Prepare for and look for work.

- Increase your earnings if you are already employed.

Here, we break down key aspects of the responsibilities tied to earnings and the thresholds that determine them.

The Administrative Earnings Threshold (AET)

The AET determines the level of earnings that influences what you are required to do under your claimant commitment.

| Status | Earnings Threshold |

|---|---|

| Individual | £892/month |

| Couple (combined) | £1,437/month |

If You Earn Below the AET

If your earnings fall below the AET, you will need to demonstrate that you are actively seeking more or better-paid work. This applies to:

- Individuals earning less than £892 per assessment period.

- Couples whose combined earnings are less than £1,437 per assessment period, where both partners must meet these obligations.

Responsibilities:

- Actively search for work opportunities or higher-paying jobs.

- Be available to start work or take on additional hours.

- Attend regular meetings with a work coach for personalised support.

How Your Work Coach Can Help:

A work coach provides tailored guidance, including:

- Job search strategies.

- Resume and interview preparation.

- Employer connections and job leads.

If You Earn Above the AET

For those earning at or above the AET:

- Individuals earning £892 or more per assessment period are exempt from actively searching for additional or higher-paid work.

- Couples with combined earnings of £1,437 or more are also exempt, meaning neither partner needs to meet the job-seeking requirements.

The Conditionality Earnings Threshold (CET)

The CET is a higher threshold than the AET, determined by the number of hours you can reasonably work given your circumstances.

What Happens if You Earn Between the AET and CET?

- You are not required to have regular meetings with a work coach.

- You can request support from your work coach if you feel it would help improve your employment situation.

If You Earn Above the CET: You are not required to have regular contact with a work coach.

Self-Employed Earnings and AET: For self-employed individuals, earnings do not count towards the AET. However, you may have other obligations under your claimant commitment, depending on your income and circumstances.

How will Universal Credit Allocated Based on Working Hours?

The number of hours you work each week and your hourly wage directly impact how much Universal Credit you can receive.

Universal Credit is designed to support those in low-income employment, with payments adjusted monthly based on your income. Let’s examine specific scenarios for working 20 hours per week and 16 hours per week at the National Minimum Wage.

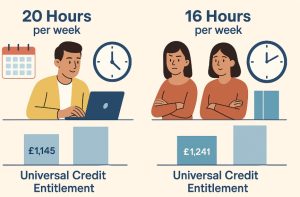

If I Work 20 Hours a Week, How Much Universal Credit Will I Get?

Scenario:

- Hourly Wage: £10/hour (assuming National Minimum Wage or above)

- Weekly Earnings: 20 hours × £10/hour = £200

- Monthly Earnings: £200 × 4.33 = £866

Work Allowance and Reduction:

- Work Allowance: £404 (if claiming the housing element)

- Excess Earnings: £866 – £404 = £462

The taper rate of 55% is applied to the excess earnings:

- Reduction = £462 × 0.55 = £254.10

Universal Credit Calculation:

If your total Universal Credit entitlement is £1,400 (including housing and other elements), the reduction would be £254.10:

- £1,400 – £254.10 = £1,145.90

So, if you work 20 hours per week at £10/hour, you could receive approximately £1,145.90/month in Universal Credit, depending on your individual circumstances.

If I Work 16 Hours a Week, How Much Universal Credit Will I Get?

Scenario:

- Hourly Wage: £10/hour

- Weekly Earnings: 16 hours × £10/hour = £160

- Monthly Earnings: £160 × 4.33 = £693

Work Allowance and Reduction:

- Work Allowance: £404 (if claiming the housing element)

- Excess Earnings: £693 – £404 = £289

The taper rate of 55% is applied to the excess earnings:

- Reduction = £289 × 0.55 = £158.95

Universal Credit Calculation:

If your total Universal Credit entitlement is £1,400, the reduction would be £158.95:

- £1,400 – £158.95 = £1,241.05

So, if you work 16 hours per week at £10/hour, you could receive approximately £1,241.05/month in Universal Credit, depending on your circumstances.

What Are the Additional Factors Affecting Payments?

Savings and Capital:

- Savings over £6,000 reduce payments (£4.35 per £250 saved).

- Savings above £16,000 make you ineligible.

Benefit Cap:

The Benefit Cap limits the total benefits you can receive. The cap applies unless:

- You or your partner earn at least £793/month.

- You’re exempt due to disability, caregiving, or other specific conditions

| Household | Monthly Cap (outside London) |

|---|---|

| Single (no children) | £1,229.42 |

| Couple or parent | £1,835.00 |

| London-based households have higher caps. |

How to Calculating Universal Credit Payments?

To calculate your Universal Credit, follow these steps:

- Start with the standard amount based on your circumstances.

- Add any additional elements, such as housing or childcare.

- Subtract reductions for earnings above the work allowance or savings above £6,000.

- Factor in the Benefit Cap, if applicable.

Online calculators like GOV.UK’s Universal Credit tool can help simplify this process.

Conclusion

Universal Credit provides a safety net for workers and families in the UK, but understanding the calculations is essential to maximise your benefit. Always report changes in income or circumstances to avoid overpayments or penalties.

For tailored advice, consult reliable resources such as GOV.UK or Citizens Advice.

FAQ

What is the taper rate for Universal Credit?

The taper rate is 55%, meaning for every £1 you earn above the work allowance, your Universal Credit reduces by 55p.

How do savings affect Universal Credit?

Savings above £6,000 reduce payments by £4.35 per £250. Savings over £16,000 disqualify you.

What happens if I work overtime?

Overtime increases your earnings, which could reduce your Universal Credit payment based on the taper rate.

Can I claim Universal Credit if I’m self-employed?

Yes, but income is assessed differently, and a minimum income floor may apply.

Does child maintenance impact Universal Credit?

No, child maintenance does not reduce Universal Credit payments.

How does the Benefit Cap affect Universal Credit?

The Benefit Cap limits your total benefits unless you meet exemption criteria, such as earning over £793/month.

What happens if my claim is reduced to zero?

If your income increases and your Universal Credit is reduced to zero, your claim may close. If your income drops within five months, you can request to reopen it.