DWP Pensioner Home Ownership Rules Changes | What You Need to Know?

What happens if a pensioner owns a home but still needs financial help? Will their property count against them when claiming benefits?

These are urgent concerns for older UK citizens, especially as the Department for Work and Pensions (DWP) has begun to reassess how property ownership interacts with pensioner benefits. Some changes are already confirmed, while others remain under review.

Understanding how these shifts affect Pension Credit, Housing Benefit, Support for Mortgage Interest (SMI), and wider property law is now essential for homeowners planning their retirement security.

What Are the Proposed DWP Changes for Pensioners Who Own Their Homes?

Under current rules, a pensioner’s primary residence is excluded when assessing entitlement to means-tested benefits like Pension Credit. However, proposed reforms for 2025–26 could introduce far-reaching changes:

-

Primary homes may be included in benefit assessments, especially for high-value properties.

-

Equity-rich households in London and the South East may face stricter scrutiny than those in lower-value regions.

-

Multiple properties (holiday homes, inherited property) are already counted, and checks are becoming stricter.

These changes are not yet law, but they reflect the government’s push for fairness, ensuring that support targets those in genuine financial need rather than those sitting on large housing wealth.

Why Is the Government Reassessing Pensioner Housing Wealth?

The government is reviewing pensioner benefits due to rising home values among retirees. Many own high-value homes yet receive means-tested support. The goal is to ensure aid goes to those truly in need, considering total assets, not just income.

Key Factors Driving Reform:

- Increasing housing wealth among retirees

- Regional differences in property values (e.g. South East vs. North West)

- Calls for fairer use of limited public funds

- Rising pressure on the benefits system

- Preventing perceived overpayment to equity-rich households

By addressing these discrepancies, the DWP aims to rebalance how support is allocated, ensuring pensioners with real financial need are prioritised.

How Is Home Ownership Currently Treated Under Pension Credit?

Currently, Pension Credit rules exclude the primary home from asset calculations. However, savings and other properties are counted.

| Capital Amount | Weekly Income Assumed |

|---|---|

| £10,000 or less | £0 |

| £11,000 | £2 |

| £12,000 | £4 |

| £13,000 | £6 |

Scenarios that affect assessments today include:

-

Owning a second property: Always included in capital.

-

Renting out a section of your home: Rental income must be declared.

-

Holding an inherited property: Even if unsold, it counts toward assets.

The government may begin including equity in the main residence in this calculation, a move that could disqualify many pensioners in high-value housing markets.

Could Support for Mortgage Interest Become More Limited?

Support for Mortgage Interest (SMI) is one of the few tools available to help pensioners with ongoing housing costs. However, it’s important to note that SMI is not a grant; it is a repayable loan.

The government covers only the interest on the mortgage, and this is calculated at a standard rate. Pensioners must repay the loan when the property is sold or their estate is settled.

With changes in means-testing rules on the horizon, the number of people qualifying for SMI might shrink, especially if home equity becomes part of capital evaluations.

Is SMI a Loan or a Grant for Pensioners?

SMI is strictly a loan, not a benefit. It helps pensioners pay the interest portion of their mortgage, but not the capital repayment.

The DWP determines the interest rate, and payments are made directly to the lender. These loans accumulate and are repayable once the property is sold or transferred.

While it helps in the short term, it creates a long-term obligation that many pensioners should carefully consider.

What Happens If the Property Is Sold After Receiving SMI?

When the property is sold, the full amount of the SMI loan, plus interest, must be repaid to the DWP. This is typically done before the distribution of any remaining proceeds from the sale.

If the sale does not cover the loan, the remaining amount may be written off, depending on individual circumstances.

However, this can reduce what is left to beneficiaries. It’s critical for homeowners considering SMI to weigh these long-term consequences.

How Will Universal Credit Affect Mixed-Age Pensioner Couples?

Universal Credit (UC) has gradually replaced legacy benefits for working-age individuals. One group especially affected by this shift is mixed-age couples, where one partner is above and the other is below State Pension age.

Key Differences in Eligibility:

- These couples must claim UC rather than Pension Credit

- UC usually offers lower support than Pension Credit

- Couples receiving income-based ESA must transition by the end of 2025

Pensioners in such relationships may face reduced payments under UC. It’s strongly advised that they seek independent advice before making changes or accepting migration notices from the DWP.

What Additional DWP Updates Will Affect Pensioner Support in 2025–2026?

Several changes already confirmed will impact how pensioners receive support, beyond the proposed homeownership reforms. These adjustments are designed to streamline systems but may also affect eligibility criteria and the application process.

Key Updates to Know:

- Housing Benefit Integration: Housing Benefit will merge with Pension Credit by 2026, simplifying applications but possibly intensifying asset checks.

- Bereavement Support Expansion: Unmarried partners with dependent children can now claim, including backdated claims.

- Disability Benefits: New claimants must apply for PIP rather than DLA. Those under 65 as of April 2013 will eventually transition to PIP.

These changes will redefine eligibility for multiple benefits and may lead to reassessments, especially involving housing or capital.

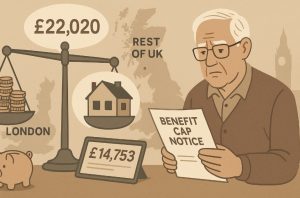

Does the Benefit Cap Still Apply to Pensioners?

The Benefit Cap limits the total amount of benefits a household can receive. While pensioners are typically exempt once they reach State Pension age, those living in mixed-age households may still be affected.

Key Points:

- Applies to those receiving Universal Credit if one partner is under pension age

- Cap levels differ based on location and household size

Pensioners should review their eligibility and partner’s circumstances to understand if the cap might impact them indirectly.

Are Pensioners in Mixed-Age Households Affected?

Yes, if one partner is below the State Pension age and claiming Universal Credit, the household could be subject to the Benefit Cap. This scenario may lead to reduced payments despite one partner being a pensioner.

This makes it critical for mixed-age couples to seek advice on whether transitioning to UC is in their best interest. Careful planning can help prevent unintended benefit reductions.

Which Benefits Exempt Pensioners from the Cap?

Certain benefits provide automatic exemptions from the cap, helping protect the most vulnerable. These include:

- Attendance Allowance

- Personal Independence Payment (PIP)

- Disability Living Allowance (DLA)

- Carer’s Allowance

- War Widow(er)’s Pension

Receiving any of these can safeguard a pensioner from the cap, ensuring they continue to receive their full entitlement without deductions.

Can Pensioners Lose Their Home Due to DWP Housing Rule Changes?

While rare, pensioners could face eviction if they no longer meet eligibility for housing assistance due to DWP rule changes. This risk increases when benefits are reassessed and found to be awarded incorrectly.

Digital verifications and home visits have become more common, especially where there are discrepancies in income reporting or living arrangements.

Ignoring DWP notices can lead to benefit suspension or even eviction in council-owned housing. To avoid this, pensioners must be vigilant about compliance and reporting changes promptly.

How Can Pensioners Prepare for Changing Housing Rules?

With rules evolving, pensioners need to act now to protect their housing and financial security. Preparation is key to avoiding shocks from reassessment or benefit loss.

Practical Steps for Preparation:

- Use official benefits calculators to understand current entitlement

- Review all sources of capital, including property and savings

- Stay compliant with DWP reporting requirements

- Seek independent advice from welfare experts before major decisions

- Avoid voluntary transitions to UC without checking the implications

By staying informed and organised, pensioners can better adapt to upcoming changes without putting their housing at risk.

How Do Wider 2025 UK Property Law Changes Affect Pensioners?

The DWP’s pensioner housing reforms are part of a much larger legal overhaul. The UK Property Law Changes 2025 affect pensioners in several ways:

-

Capital Gains Tax Updates: HMRC has updated rules on Private Residence Relief, affecting pensioners selling their homes.

-

Mortgage Rule Reforms: The FCA is modernising later-life borrowing, affecting retirees looking for equity release.

-

Stamp Duty Changes: The nil-rate threshold dropped from £250,000 to £125,000 in April 2025, increasing costs for downsizers.

These changes show that pensioners must now consider taxation, welfare, and property law together when planning finances.

Conclusion

The UK pensioner benefits landscape is undergoing its most dramatic shift in decades. With DWP home ownership rule changes, SMI loan adjustments, Housing Benefit integration, and wider property law reforms, pensioners must plan carefully.

Owning a home may soon count directly against benefit eligibility, particularly for those with high-value properties. Preparing early, by reviewing capital, seeking advice, and exploring downsizing, can help pensioners secure their financial stability while adapting to a stricter system.

FAQs About DWP Pensioner Home Ownership Rules Changes

Will home improvements affect my benefit entitlement?

Yes, if they are funded through savings or loans, they may be considered capital and could impact means-tested benefits.

Are pensioners required to report short-term absences from their homes?

Yes. Absences longer than four weeks should be reported to the DWP to avoid breaching benefit terms.

What should pensioners do if they receive a DWP compliance letter?

Respond promptly, seek help from a welfare advisor, and gather documentation to support your claims.

How do these changes affect council tax support for pensioners?

While assessed separately, changes in income or capital can indirectly affect council tax reductions.

What happens if a pensioner inherits a home while claiming benefits?

It may be assessed as capital, depending on whether it’s lived in, rented, or sold, potentially affecting entitlement.

Can pensioners appeal a benefit decision made under the new rules?

Yes. Appeals can be made through the DWP or supported by local authorities, Age UK, or Citizens Advice.

Do these changes affect service charge support for homeowners?

Yes. Pensioners receiving help with service charges may face stricter checks on household income and residency status.

Read Next:

If My Universal Credit is Due on a Sunday, When Will I Get It?

DWP Moving House Grant: What It Is and How to Apply in the UK?