Universal Credit Under 25 Penalty: The £338 vs £425 Gap Explained

If you have heard people talk about a Universal Credit under 25 penalty, they are usually referring to the lower standard allowance paid to younger claimants.

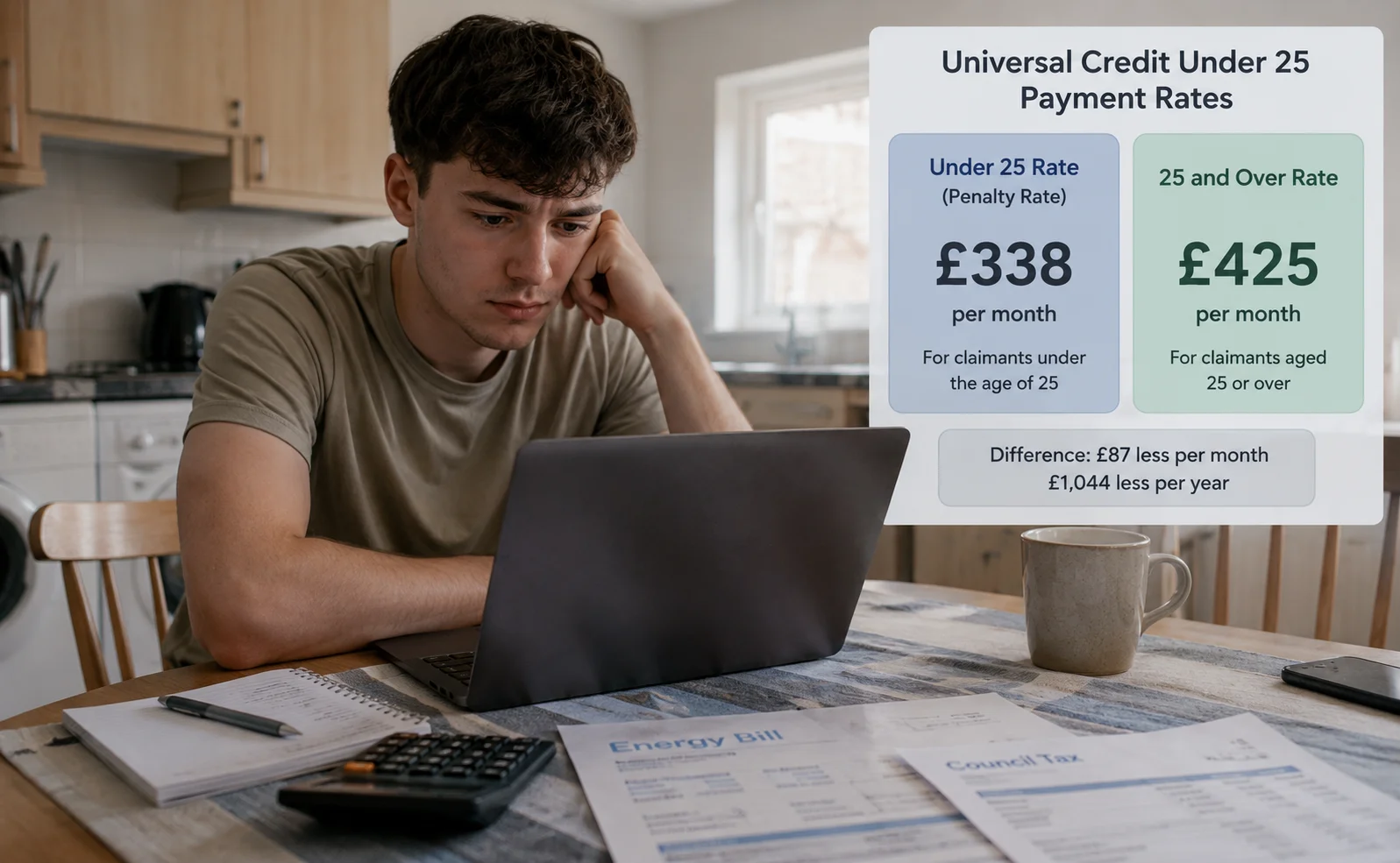

In 2026, a single person under 25 receives £338.58 per month, while someone aged 25 or over receives £424.90, creating a noticeable gap in support.

Although this is an official DWP policy rather than a formal penalty, many campaigners argue that younger adults face the same living costs as older claimants.

Key points:

- Single claimants under 25 receive £338.58 per month.

- Single claimants aged 25 and over receive £424.90 per month.

- The difference is £86.32 per month.

- Additional elements may increase your Universal Credit entitlement.

- Sanctions and deductions can further reduce payments.

- Hardship Payments may be available in certain circumstances.

What Is the Universal Credit Under 25 Penalty?

The term Universal Credit under 25 penalty is widely used by campaigners, benefits advisers and claimants to describe the lower standard allowance paid to younger adults.

Under current Universal Credit rules, age is one of the factors used to determine the standard allowance. If you are single and under 25, you receive a lower monthly payment than a claimant who is 25 or older.

The policy has been debated for years because many people argue that rent, food, energy bills and transport costs do not automatically become cheaper simply because someone is younger.

“Universal Credit uses age-based standard allowances, but entitlement can increase significantly where additional needs such as housing, childcare or disability apply.” — DWP Benefits Guidance

While critics often call it a penalty, the Department for Work and Pensions (DWP) considers it part of the Universal Credit structure rather than a financial punishment.

Why Do Under-25s Get £338.58 While Over-25s Get £424.90?

The Government’s position has historically been that younger adults may have different living circumstances and potentially greater access to family support than older claimants.

However, this reasoning has faced criticism from welfare organisations and anti-poverty groups. Many argue that younger adults often face the same financial pressures as older claimants, particularly in areas with high housing costs.

Campaigners have also highlighted concerns about young parents, noting that the cost of raising children does not vary based on the age of the parent.

The DWP has responded by pointing out that Universal Credit includes additional elements for housing, childcare, children, caring responsibilities and health conditions, which can substantially increase overall support beyond the standard allowance.

How Much Is the Universal Credit Age Gap in 2026?

The difference between Universal Credit payments for those under 25 and those aged 25 or over remains a widely discussed aspect of the benefits system.

While additional Universal Credit elements may provide extra support, the standard allowance is lower for younger claimants.

Single Claimant Rate Comparison

For single claimants, turning 25 leads to a noticeable increase in the standard allowance.

| Claimant Type | Monthly Allowance |

|---|---|

| Single under 25 | £338.58 |

| Single aged 25 or over | £424.90 |

| Difference | £86.32 |

Although £86.32 may seem small each month, it can make a meaningful difference to younger adults managing everyday living costs.

Couple Claimant Rate Comparison

The gap is even larger for couples, where households with both partners under 25 receive a lower allowance.

| Household Type | Monthly Allowance |

|---|---|

| Both partners under 25 | £528.34 |

| One or both partners aged 25 or over | £666.97 |

| Difference | £138.63 |

For younger couples, this difference can have a significant impact on household budgets and living expenses.

Monthly and Annual Difference

Looking at the yearly figures highlights the financial impact more clearly.

| Comparison | Monthly Gap | Annual Gap |

|---|---|---|

| Single claimant | £86.32 | £1,035.84 |

| Couple claimants | £138.63 | £1,663.56 |

A single claimant under 25 receives over £1,000 less per year than someone aged 25 or over, while younger couples receive more than £1,600 less annually.

These figures continue to fuel debate about whether the current age-based structure reflects the true cost of living for younger adults.

Is the Universal Credit Under 25 Rate the Same as a Sanction?

No. This is one of the most common misunderstandings among claimants. The lower payment for under-25s is a standard part of Universal Credit rules.

A sanction is a completely separate reduction applied when a claimant fails to meet agreed conditions without a valid reason.

For example, sanctions may occur if you:

- Miss a mandatory appointment.

- Fail to complete agreed work-search activities.

- Do not comply with your claimant commitment.

- Refuse suitable work opportunities without good reason.

A sanction can reduce your payment by up to 100% of your daily standard allowance for the period it applies. In severe cases, this could leave a claimant receiving very little or no standard allowance during the sanction period.

Understanding the distinction between age-related rates and sanctions is essential when reviewing your Universal Credit statement.

When Can Your Universal Credit Be Reduced Further?

Beyond the lower under-25 allowance, there are several situations where your Universal Credit payment may be reduced. In many cases, reductions are linked to claimant responsibilities or deductions that are applied directly to your award.

Sanctions for Missing Claimant Commitment Rules

Every claimant is required to agree to a claimant commitment outlining work-related expectations. If you fail to meet these responsibilities without a valid reason, the DWP may impose a sanction.

Common triggers include missed appointments, inadequate job-search activity or failure to participate in required work-related programmes.

“Sanctions are intended to encourage compliance with agreed commitments, but claimants should always explain any circumstances that prevented attendance or participation.” — Universal Credit Work Coach Guidance

Sanctions are assessed individually, and claimants can request a mandatory reconsideration if they disagree with a decision.

Deductions for Advances, Overpayments and Debts

Many claimants see reductions due to deductions rather than sanctions. These amounts are taken directly from monthly Universal Credit payments.

Common deductions include:

- Universal Credit advance repayments.

- Previous benefit overpayments.

- Council Tax arrears.

- Court fines.

- Utility debt repayments.

- Child Maintenance obligations.

These deductions can significantly affect the final amount received each month. Checking your Universal Credit statement regularly can help identify exactly why money has been deducted.

What Extra Universal Credit Support Can You Get Under 25?

Although younger claimants receive a lower standard allowance, many may qualify for additional support depending on their circumstances.

Additional Universal Credit elements can include housing support, childcare assistance, disability-related payments and carer support.

Available additional support:

- Child element payments.

- Housing cost contributions.

- Childcare support of up to 85% of eligible costs.

- Limited Capability for Work payments.

- Carer’s Element.

- Transitional protection in certain cases.

For many households, these additions can increase entitlement substantially above the basic standard allowance. Therefore, focusing solely on the under-25 standard rate may not provide a complete picture of your potential entitlement.

How Does the Under-25 Rule Affect Young Parents?

The under-25 Universal Credit rule is often debated when it comes to young parents. While younger claimants receive a lower standard allowance, parents may still qualify for additional support that can significantly increase their overall entitlement.

Child Element and Childcare Support

Parents receiving Universal Credit may be eligible for extra financial support regardless of age. Current support can include:

- £303.94 per month for each eligible child

- Additional disability-related child elements

- Up to 85% reimbursement of eligible childcare costs

- Housing support based on individual circumstances

These additional elements can substantially increase household income and help with the costs of raising children.

Why Campaigners Call It a Young Parent Penalty?

Many campaign groups argue that younger parents face the same childcare, food, clothing, and housing costs as older parents but receive a lower standard allowance because of their age.

“The costs of raising children do not decrease because a parent is under 25, which is why many organisations continue to call for reform.” — Child Poverty Policy Advocate

Supporters of reform believe the current structure places additional financial pressure on younger families, making this one of the most debated aspects of the Universal Credit system.

What Can You Do If Your Universal Credit Payment Is Too Low?

If your Universal Credit payment seems lower than expected, it is important to review your statement carefully before assuming an error has occurred.

Many payment differences are linked to missing information, deductions, or changes in personal circumstances.

Important Things to Check:

- Age category: Ensure the correct age-related allowance has been applied.

- Housing costs: Check that eligible rent or housing support is included.

- Child-related elements: Confirm support for eligible children has been added.

- Disability or caring responsibilities: Make sure relevant information has been reported.

- Deductions or sanctions: Review whether repayments or sanctions are reducing your award.

If you are experiencing financial hardship because of a sanction, you may be eligible for a Hardship Payment, although this is usually repaid through future deductions.

Seeking advice from Citizens Advice or a welfare rights adviser can also help ensure you receive all the support you are entitled to claim.

How Can You Check Whether Your Universal Credit Payment Is Correct?

The most reliable way to verify your entitlement is by reviewing your Universal Credit online account and comparing your payment breakdown against current DWP rules.

You should also report any changes in circumstances promptly, including:

- Starting work.

- Moving home.

- Becoming a parent.

- Developing a health condition.

- Taking on caring responsibilities.

- Changes to your household composition.

Many additional elements are not applied automatically, meaning delays in reporting changes could result in missed entitlement.

By understanding the rules surrounding the Universal Credit under 25 penalty, sanctions and additional support elements, you can better assess whether your payment accurately reflects your circumstances.

Final Thoughts

The Universal Credit under 25 penalty refers to the lower standard allowance paid to younger claimants, resulting in a gap of £86.32 per month for single adults and £138.63 for eligible couples.

While additional elements for housing, children, disability and caring responsibilities can increase support, the age-based difference remains controversial.

Understanding your entitlement, checking for deductions and reporting changes promptly can help ensure you receive the correct Universal Credit payment.

Frequently Asked Questions

Can you get the higher Universal Credit rate before turning 25?

In most cases, the higher single claimant standard allowance applies once you reach age 25. Before then, the under-25 rate normally applies unless specific entitlement rules affect your claim.

Does Universal Credit increase automatically when you turn 25?

Yes. The DWP should apply the appropriate age-related standard allowance when you become eligible for the higher rate.

Can an under-25 claimant get help with rent?

Yes. Housing support may be available through the housing costs element of Universal Credit, depending on your circumstances.

What happens if a sanction leaves you with no money?

You may be able to apply for a Hardship Payment if you meet the eligibility requirements and are unable to cover essential living costs.

Can you challenge a Universal Credit sanction?

Yes. You can request a mandatory reconsideration if you believe a sanction decision was incorrect.

Do savings affect Universal Credit for under-25s?

Yes. Savings above certain thresholds can reduce entitlement, and claims are generally not available where savings exceed £16,000.

Can working under-25s still claim Universal Credit?

Yes. Universal Credit can support people who are employed but have a low income, provided they meet eligibility requirements.