How Much Savings You Can Have on Universal Credit in 2026?

If you are claiming Universal Credit or thinking about applying in 2026, one of the most important questions is how much savings you can have before your payments are affected.

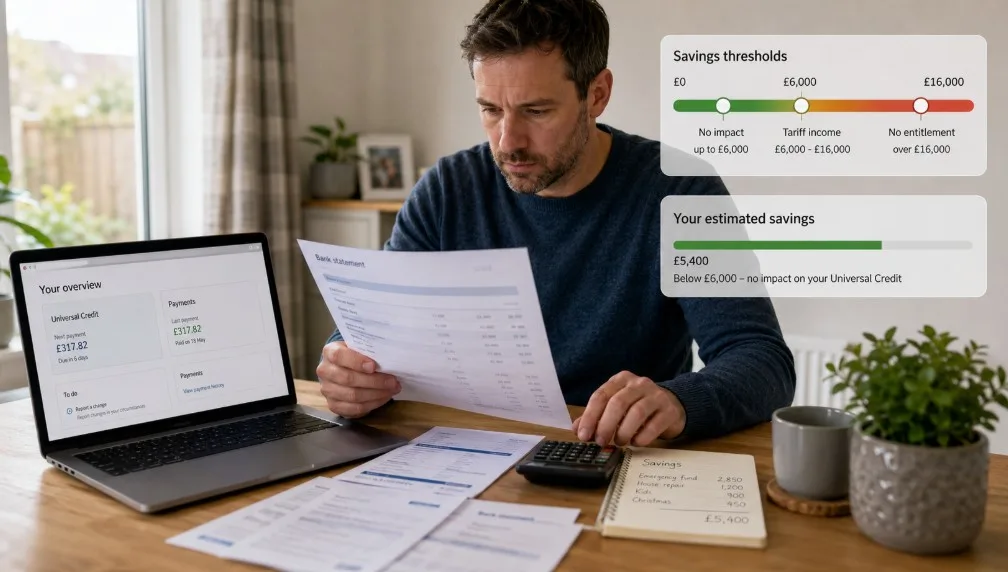

In most cases, you can have up to £16,000 in savings or capital and still be eligible for Universal Credit, but the amount you receive changes depending on your total savings. Savings below £6,000 are ignored, while savings between £6,000 and £16,000 reduce your monthly award.

Key highlights:

- Savings under £6,000 do not affect Universal Credit

- Savings from £6,000 to £16,000 reduce payments

- Savings over £16,000 usually stop entitlement

- Your partner’s savings count if you claim together

Understanding these rules can help you avoid payment issues and make informed financial decisions.

How Much Savings Can You Have on Universal Credit in 2026?

Universal Credit is a means-tested benefit, which means your entitlement depends partly on the amount of money, savings and investments available to your household.

The key savings thresholds remain central to how claims are assessed and understanding these limits can help you avoid unexpected changes to your monthly award.

Universal Credit Savings Limits in 2026:

| Total Savings or Capital | Impact on Universal Credit |

|---|---|

| Less than £6,000 | No effect on payments |

| £6,000 to £16,000 | Payments reduce |

| More than £16,000 | Usually not eligible |

Savings include more than money sitting in a savings account. The DWP may assess available capital including cash, investments and certain property holdings.

If you make a joint claim, your combined household savings are considered rather than individual balances.

“Universal Credit is designed to target support according to household circumstances, including available capital and financial resources.” — DWP guidance summary

Understanding where your savings sit within these thresholds helps you estimate whether your Universal Credit payments will remain unchanged or reduce over time.

What Is Universal Credit and Who Can Claim It?

Universal Credit is a UK social security payment created to support working-age people with living and housing costs. It replaced several older benefits into one monthly payment.

You may claim Universal Credit if you:

- are on a low income

- are unemployed

- are working but earning below required thresholds

- cannot work because of illness or disability

- care for another person

Your monthly award starts with a standard allowance and may increase depending on personal circumstances.

Additional support may include:

- housing costs

- childcare support

- child elements

- disability support

- carer support

Universal Credit is normally paid monthly into your bank or building society account and is designed to adjust as your financial situation changes. Although earnings can reduce payments gradually, being employed does not automatically stop your claim.

What Happens If Your Savings Are Between £6,000 and £16,000?

Once your savings exceed £6,000, Universal Credit starts applying what is commonly referred to as tariff income. Rather than assuming you spend those savings directly, the DWP treats part of the amount above £6,000 as producing monthly income.

The current calculation reduces your payment by £4.35 per month for every £250 (or part of £250) above the threshold.

Example of Savings Reductions:

| Savings | Amount Above £6,000 | Reduction Applied |

|---|---|---|

| £6,000 | £0 | £0 |

| £7,000 | £1,000 | £17.40 |

| £10,000 | £4,000 | £69.60 |

| £15,000 | £9,000 | £156.60 |

Example calculation:

A claimant has £7,000 saved.

- Step 1: £7,000 − £6,000 = £1,000

- Step 2: £1,000 ÷ £250 = 4

- Step 3: 4 × £4.35 = £17.40 deduction

These deductions are automatically reflected in your monthly statement and can change if your savings increase or decrease.

Checking your online statements regularly helps ensure calculations reflect your actual circumstances.

Can You Claim Universal Credit If You Have More Than £16,000?

For most claimants, having more than £16,000 in savings means you are not entitled to Universal Credit. However, there is an important exception that some households overlook.

If you moved from tax credits to Universal Credit after receiving a migration notice, transitional rules may allow you to keep savings above £16,000 for up to 12 months from the start of your claim.

If savings remain above that limit after the transitional period ends, entitlement generally stops. This protection does not normally apply if you chose to move voluntarily before receiving a migration notice.

“Capital rules exist to maintain consistency across means-tested support and ensure awards reflect available financial resources.” — Benefits policy interpretation

Before assuming you are ineligible, always check whether migration protections or specific circumstances apply to your claim.

What Counts as Savings or Capital for Universal Credit?

When assessing your Universal Credit claim, the DWP looks at your total savings and capital rather than only the money in your main bank account. This assessment helps determine whether your payments stay the same, reduce, or stop altogether.

Understanding what is included can help you report your finances correctly and avoid unexpected changes to your entitlement.

Which Types of Money and Investments Count?

The DWP uses a broad definition of savings and capital. Many people underestimate what may be included during assessment because it extends beyond standard bank accounts.

Examples include:

- cash

- current accounts

- savings accounts

- building society balances

- credit union accounts

- ISAs

- stocks and shares

- Premium Bonds

- PayPal balances

- cryptocurrency holdings

Property and Household Capital Rules

Property that you do not live in can sometimes be counted as capital and assessed differently depending on ownership and usage.

If you claim as a couple, your partner’s savings are also included in the total household calculation. Money held for another person may still be reviewed depending on ownership and access arrangements.

What Usually Counts and Does Not Count:

| Counts as Savings | Usually Ignored |

|---|---|

| Bank accounts | Main home |

| ISAs | Pension pots |

| Investments | Child trust funds |

| Premium Bonds | Personal possessions |

| Cryptocurrency | Furniture |

These rules make it important to review all available assets rather than focusing only on traditional savings accounts.

What Does Not Count as Savings for Universal Credit?

Not all assets affect your Universal Credit claim and understanding exclusions can prevent unnecessary concern. Certain forms of capital are excluded because they are treated differently under benefit regulations.

Examples that are generally ignored include:

- the home you live in

- pension funds not yet accessed

- life insurance policies

- children’s bank accounts

- child trust funds

- personal items such as cars, jewellery and household furniture

Many claimants worry unnecessarily about possessions or pension values when these may not reduce their payments. Even so, exceptions can apply in specific situations, so keeping records remains sensible.

When Do Wages Become Savings on Universal Credit?

Income and savings are not treated the same way under Universal Credit. When you receive wages, they are initially treated as earnings. If part of those wages remains unspent after your next assessment period, they may then become capital.

Consider a simplified example.

You receive your salary during one assessment period but keep most of it in your account beyond the following period. At that stage, remaining funds may count as savings.

Real-time claimant insight:

A claimant shared that after receiving overtime and leaving the extra money untouched for several weeks, they were surprised when Universal Credit later requested updated savings information.

Their concern was not the payment reduction itself but understanding when earnings changed into capital. The experience highlighted how easy it is to assume wages and savings are assessed separately indefinitely.

Reviewing statements and reporting changes early helped avoid confusion and prevented adjustments later in the claim.

This example shows why timing matters as much as the amount saved.

How Do You Report Savings Changes to the DWP?

Reporting savings changes to the DWP is an important part of managing your Universal Credit claim. Your payments are based on your financial circumstances, so any increase or change in savings, investments or capital should be updated promptly.

Keeping your information accurate helps ensure you receive the correct entitlement and reduces the risk of future payment adjustments.

What Changes Must You Tell Universal Credit About?

When you apply for Universal Credit, you provide details about your finances, but reporting duties continue during your claim. You should update the DWP whenever there is a significant change to your available capital.

Examples of changes to report:

- inheritance

- redundancy payments

- compensation settlements

- divorce settlements

- pension lump sums

- life insurance payments

- increased savings

Failure to report changes may lead to:

- overpayments

- underpayments

- investigations

- penalties

Reporting Through Your Universal Credit Account

Most updates can be completed through your online Universal Credit account. Table: Common Changes That Should Be Reported

| Change | Why It Matters |

|---|---|

| Inheritance | May increase capital |

| Redundancy payment | Could alter entitlement |

| Compensation | May affect assessment |

| Increased savings | Could reduce payments |

“Accurate and timely reporting supports correct benefit payments and reduces avoidable reassessments.” — Welfare administration guidance

Keeping your information updated helps maintain accurate payments and reduces administrative delays.

Can You Spend Savings Without Affecting Your Universal Credit?

Having savings does not mean you cannot use your money. The DWP recognises that people spend money for legitimate reasons.

Reasonable examples may include:

- paying off debts

- replacing essential household items

- managing living costs

- covering necessary expenses

However, deliberately reducing savings to qualify for higher benefits is known as deprivation of capital.

If the DWP decides you intentionally gave money away or spent unusually to increase entitlement, they may:

- refuse your claim

- calculate your Universal Credit as though you still hold the savings

The purpose of these rules is not to prevent normal spending but to discourage intentional manipulation of eligibility. Ending note: Keeping receipts and maintaining clear records can help explain legitimate spending decisions if questions arise later.

What Should You Remember About Universal Credit Savings Limits in 2026?

Understanding Universal Credit savings rules is less about avoiding savings and more about understanding how capital affects entitlement.

The key figures remain straightforward:

- Up to £6,000 → ignored

- £6,000–£16,000 → payment reduction

- Over £16,000 → usually no entitlement

You should also remember:

- partner savings count

- wages can become savings later

- report changes promptly

- avoid deprivation of capital

- check statements regularly

If your circumstances are complex, using a recognised benefits calculator or checking official guidance can help you estimate outcomes before making financial decisions.

Conclusion

If you are wondering how much savings you can have on Universal Credit in 2026, the general answer is up to £16,000, although payments begin reducing once your savings go above £6,000. The rules apply across cash, investments and other forms of capital, and joint claims include your partner’s finances.

Understanding what counts, what does not count, and when to report changes can help you protect your entitlement and avoid unnecessary payment issues.

FAQs About Universal Credit Savings

Does Universal Credit check your bank balance automatically?

Universal Credit may ask for evidence of savings and financial information during reviews or claim assessments.

Can savings in a joint account affect Universal Credit?

Yes. Joint account balances may be considered when calculating household capital.

Does receiving a gift affect Universal Credit entitlement?

Large gifts may count as capital depending on how they are held and used.

Are Premium Bonds treated differently from cash savings?

No. Premium Bonds are generally considered capital.

Can you challenge a Universal Credit capital decision?

Yes. You can request a mandatory reconsideration if you disagree.

How often should you review your Universal Credit statement?

Review statements whenever savings, income or circumstances change.

Does owning cryptocurrency affect benefit calculations?

Yes. Cryptocurrency may be treated as savings or investments.