What is Universal Credit in the UK? | A Complete Guide

Universal Credit (UC) is one of the most significant welfare reforms in the UK in recent decades. Introduced to simplify a complex benefits system, it aims to provide financial support to individuals and families on a low income or those out of work.

This guide explores what is Universal Credit, its objectives, how it works, who is eligible, and its advantages and challenges in detail.

What Is Universal Credit?

Universal Credit is a means-tested benefit introduced in 2013 to replace six existing benefits, collectively known as “legacy benefits.” These are:

- Income Support (IS): Support for those with low income and limited ability to work.

- Income-based Jobseeker’s Allowance (JSA): Financial assistance for unemployed individuals actively seeking work.

- Income-related Employment and Support Allowance (ESA): Aid for individuals unable to work due to illness or disability.

- Housing Benefit: Assistance with housing costs for low-income renters.

- Child Tax Credit: Financial support for families with dependent children.

- Working Tax Credit: Aimed at supporting individuals in low-income employment.

Universal Credit consolidates these benefits into a single monthly payment. The primary goal is to simplify the system, reduce administrative costs, and ensure claimants receive appropriate support.

Why Was Universal Credit Introduced?

The government introduced Universal Credit to address several issues with the previous system:

- Simplification: The old system was complex, with overlapping benefits and multiple agencies handling claims. UC simplifies this with a single application and payment.

- Encouraging Employment: UC aims to ensure people are always better off working. Payments reduce gradually as you earn more, avoiding “cliff edges” where claimants lost benefits abruptly.

- Supporting Modern Work Patterns: The system is designed to adapt to flexible and irregular work schedules, such as zero-hours contracts or freelance work.

- Reducing Administrative Costs: Combining benefits into one system helps cut administrative overheads and inefficiencies.

Who Is Eligible for Universal Credit?

Eligibility for Universal Credit depends on several factors:

- Age: You must be over 18 but under State Pension age. There are exceptions for 16- and 17-year-olds in specific circumstances, such as being responsible for a child.

- Residency: You must live in the UK and meet immigration status requirements.

- Savings and Income: Savings over £16,000 disqualify you, while savings between £6,000 and £16,000 reduce your entitlement. Your household income is also considered.

- Employment Status: Whether you’re unemployed, working, or self-employed, you may still qualify, though your earnings will affect your payment.

- Housing and Family Circumstances: Dependents, housing costs, and other factors can influence your claim.

How Are Universal Credit Payments Calculated?

Universal Credit payments depend on your personal circumstances, including your age, living arrangements, and income.

Standard Allowance (Monthly Payment)

As of the latest rates:

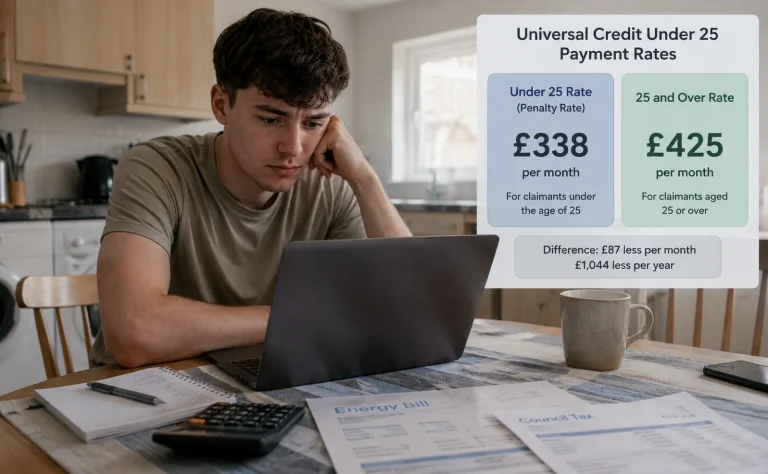

- If you’re single and under 25: £311.68

- If you’re single and 25 or over: £393.45

- If you live with your partner and you’re both under 25: £489.23 (for both)

- If you live with your partner and either of you are 25 or over: £617.60 (for both)

Additional Elements

You may receive extra payments depending on your needs:

- Child Element: Support for children under 18 or disabled children.

- Housing Element: Helps with rent or mortgage interest.

- Disability and Carer Elements: Additional funds for claimants with disabilities or caring responsibilities.

- Work Allowances: Lets you earn a set amount before UC payments are reduced.

Adjustments for Income

UC payments decrease as you earn more, following a taper rate of 55%. For every £1 you earn above your work allowance (if applicable), your UC payment reduces by 55p.

How Do You Apply for Universal Credit?

The process of applying for Universal Credit (UC) is designed to be straightforward but requires careful preparation and attention to detail. Here’s a detailed breakdown of the application process:

Step 1: Online Application

Universal Credit applications are primarily conducted online through the UK government’s UC portal. You’ll need to create an account and complete the application form. This includes providing personal information such as:

- Your full name, date of birth, and National Insurance number.

- Your housing details, including your rent or mortgage costs.

- Information about your income, savings, and any existing benefits.

- The number of people in your household, including dependents.

Step 2: Provide Detailed Information

Applicants are required to submit evidence of their circumstances to determine eligibility. This includes documentation like:

- Bank statements to verify financial activity.

- Pay slips or proof of income if you’re employed or self-employed.

- Housing agreements or mortgage statements for proof of housing costs.

- Identification documents (passport, driving license, or birth certificate) for yourself and dependents.

Step 3: Identity Verification

Claimants must verify their identity either online or in-person. Online verification may require uploading photos of ID documents, while in-person verification involves attending a local Jobcentre.

Step 4: Jobcentre Appointment

Once your online application is submitted, you’ll be invited to attend a meeting at your local Jobcentre. During this meeting, you’ll discuss your claim with a work coach and agree to a ‘Claimant Commitment.’

This document outlines the actions you’ll take to improve your situation, such as actively seeking work, training, or education. Fulfilling this commitment is essential to continue receiving payments.

Step 5: Wait for Your First Payment

After completing your application and assessment, your first Universal Credit payment is typically made five weeks later.

This includes a four-week assessment period and one week for processing. If you face financial hardship during this waiting period, you can apply for an advance payment, which is later deducted from your monthly payments.

How Does Universal Credit Work?

Universal Credit is designed to adapt to individual circumstances and ensure claimants receive the right level of support.

Monthly Payments

UC payments are made monthly, directly into your bank account. This mirrors how most salaries are paid, encouraging claimants to manage their finances in a similar way.

Assessment Period

Your UC payment is calculated based on an assessment period, which is a calendar month. During this time, the government reviews your income, housing costs, and personal circumstances.

Changes, such as an increase in earnings or a change in family size, are reflected in the next payment.

Adjustments for Earnings

UC payments are means-tested, meaning they decrease as your income increases. For every £1 you earn above your work allowance (if applicable), your payment is reduced by 55p. This taper rate ensures that claimants are always better off working.

Additional Elements

UC adapts to specific needs by offering additional payments for:

- Childcare costs.

- Disabilities or long-term health conditions.

- Housing costs, including rent and mortgage interest.

Managing Changes

If your circumstances change, such as starting a new job, having a child, or moving house, you must report these changes promptly to avoid overpayments or underpayments.

What Are the Benefits of Universal Credit?

Universal Credit offers several advantages compared to the previous system of legacy benefits:

Simplification of the System

Replacing six separate benefits with one payment streamlines the process for claimants and administrators. It reduces the need for multiple applications and simplifies changes in circumstances.

Encouraging Employment

UC’s gradual taper system ensures that claimants are always better off working. Unlike the abrupt withdrawal of legacy benefits, UC reduces payments progressively as earnings increase.

Flexibility and Adaptability

The monthly assessment period ensures that UC reflects current circumstances. For example, if a claimant’s income decreases, their UC payment will increase in the next assessment period. This adaptability is particularly beneficial for those with fluctuating incomes, such as freelancers or gig economy workers.

Holistic Support

UC provides a single platform for addressing various needs, including housing, childcare, and disabilities. This ensures claimants receive comprehensive support tailored to their situation.

Financial Independence

Monthly payments mimic a typical salary structure, encouraging claimants to manage their finances effectively. This can help them transition smoothly into employment.

What Are the Criticisms of Universal Credit?

Despite its benefits, Universal Credit has faced significant criticism since its introduction:

Delays in Payments

One of the most frequent complaints about UC is the five-week wait for the first payment. This delay has caused financial hardship for many claimants, leading to reliance on food banks and payday loans.

While advance payments are available, they must be repaid, reducing future payments and adding financial pressure.

Impact on Vulnerable Groups

Critics argue that UC disproportionately affects vulnerable populations, including single parents, disabled individuals, and the homeless. For example:

- Single parents often struggle with reduced income and increased childcare costs.

- Disabled claimants may find the transition to UC particularly challenging due to the loss of certain benefits like Severe Disability Premium.

Digital Exclusion

UC’s online-only application system creates barriers for claimants without internet access or digital skills. This particularly affects older individuals, those in rural areas, or people experiencing homelessness.

Sanctions and Strict Requirements

The ‘Claimant Commitment’ requires claimants to meet specific conditions, such as attending Jobcentre appointments or applying for jobs. Failure to comply can result in sanctions, leading to reduced or suspended payments. Critics argue that this approach is punitive and fails to account for individual circumstances.

How Did the COVID-19 Pandemic Impact Universal Credit?

The COVID-19 pandemic highlighted the importance of Universal Credit as millions of people turned to the system for support during lockdowns and widespread job losses. Key impacts included:

Surge in Applications

The number of UC claimants skyrocketed during the pandemic, putting immense pressure on the system. Between March and May 2020 alone, nearly 3 million people applied for UC.

Temporary Uplift

To help struggling households, the government introduced a £20-per-week uplift to UC payments. This temporary measure provided much-needed relief but was withdrawn in October 2021, sparking widespread criticism from claimants and anti-poverty organizations.

Highlighting Inequalities

The pandemic underscored existing weaknesses in the welfare system, including the inadequacy of standard UC payments to meet rising living costs. It also highlighted the challenges faced by gig economy workers and others with unstable incomes.

What’s the Future of Universal Credit?

As Universal Credit continues to evolve, there are ongoing debates and proposals about how to improve the system:

Reducing the Five-Week Wait

Many policymakers and advocacy groups are pushing for a shorter waiting period for first payments. Alternatives include upfront grants instead of repayable advances.

Increasing the Standard Allowance

With inflation and the cost of living rising, there are calls to permanently increase UC payments to provide more meaningful support to low-income households.

Enhancing Digital Access

To address digital exclusion, the government may invest in programs to improve internet access and digital literacy among claimants.

Simplifying the Transition

Reforms could include more targeted support for claimants moving from legacy benefits, particularly those with complex needs or disabilities.

Addressing Criticisms of Sanctions

Future reforms may aim to make the ‘Claimant Commitment’ more flexible, focusing on supportive rather than punitive measures.

Universal Credit has the potential to be a cornerstone of the UK’s welfare system. However, its success depends on addressing the criticisms and adapting to the needs of a changing society.

Final Thoughts

Universal Credit is a transformative yet controversial welfare reform. While it simplifies and modernizes benefits, challenges like delays, digital barriers, and adequacy of support remain.

Understanding the system’s workings, benefits, and criticisms is crucial for claimants and policymakers alike. As the system evolves, ensuring it meets the needs of all claimants will be vital to its long-term success.

FAQ

What benefits does Universal Credit replace?

Universal Credit replaces six legacy benefits: Child Tax Credit, Housing Benefit, Income Support, income-based Jobseeker’s Allowance, income-related Employment and Support Allowance, and Working Tax Credit.

Can I still receive other benefits alongside Universal Credit?

Yes, you can receive other benefits like Personal Independence Payment (PIP), Carer’s Allowance, or Disability Living Allowance (DLA) alongside Universal Credit, as they are not means-tested.

What is the Claimant Commitment?

The Claimant Commitment is an agreement between you and your work coach that outlines the actions you’ll take, such as job applications or training, to continue receiving Universal Credit.

What happens if I don’t meet the Claimant Commitment?

If you fail to meet the terms of your Claimant Commitment without a valid reason, your Universal Credit payments may be reduced or stopped, a process known as a sanction.

Can I apply for Universal Credit if I’m self-employed?

Yes, self-employed individuals can apply for Universal Credit. However, payments are assessed based on a “minimum income floor,” which assumes a certain level of earnings, even if your actual income is lower.

What is the five-week wait for Universal Credit payments?

The five-week wait includes a four-week assessment period and one week for processing your first payment. If needed, you can request an advance, but it must be repaid from future payments.

What is the taper rate in Universal Credit?

The taper rate is 55%, meaning for every £1 you earn above your work allowance, your Universal Credit payment is reduced by 55p, ensuring you’re always better off working.

Can I claim Universal Credit if I have savings?

You can claim Universal Credit if your savings are below £16,000. However, savings between £6,000 and £16,000 will reduce the amount you receive.

How does Universal Credit help with housing costs?

Universal Credit includes a housing element to help with rent or mortgage interest payments. The amount depends on your circumstances, such as your housing costs and location.

What happens if my circumstances change while claiming Universal Credit?

You must report changes like a new job, moving house, or a change in household size. Universal Credit will adjust your payment to reflect your new circumstances in the next assessment period.