What Counts as Savings for Universal Credit?

Universal Credit is a key part of the UK’s benefits system, designed to provide financial support to those who are out of work or on a low income. However, not everyone qualifies, and one of the most significant factors affecting eligibility is how much you have in savings and capital.

For many, the question of what counts as savings for Universal Credit can be confusing, particularly with the wide range of assets and income types considered.

Whether it’s money in the bank, an inheritance, or a second property, understanding what’s included in your total capital can make all the difference when applying or managing an existing claim.

In this detailed guide, we break down the rules around savings and Universal Credit, including what’s counted, what’s not, how it affects your payments, and what to do if your financial circumstances change.

Why Does Universal Credit Consider Savings and Capital?

The purpose of assessing capital is to ensure Universal Credit supports those who need it most. The government sets savings limits to balance financial support with personal responsibility. If someone has sufficient resources to meet their living costs, they are expected to use those before relying on public funds.

Savings are viewed as a financial cushion. If an individual or household has substantial savings or investments, these assets can be used, at least in the short term, to supplement income. For this reason, capital is factored into both eligibility and the amount you receive under Universal Credit.

This helps prevent overpayments and ensures the integrity of the benefits system by targeting support appropriately.

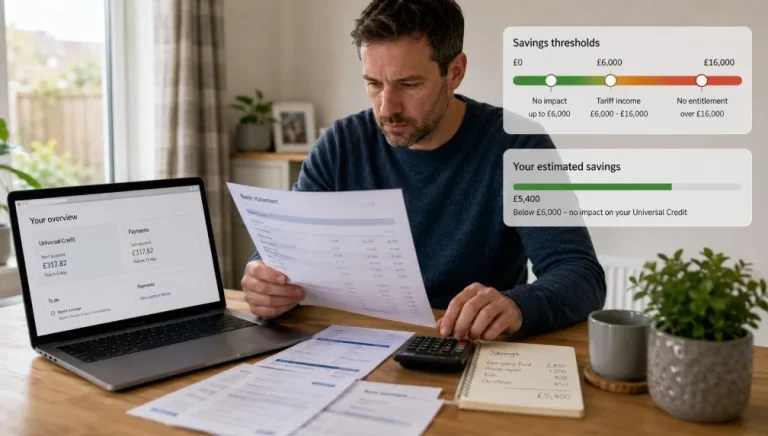

How Much in Savings Can You Have Before Universal Credit Is Affected?

Understanding the savings thresholds is crucial for anyone applying for or currently receiving Universal Credit. The UK government uses two main capital thresholds to assess how much financial support you are eligible for:

- Up to £6,000: No impact on your Universal Credit payments.

- £6,000 to £16,000: Your payment is reduced by £4.35 per month for every £250 (or part of £250) above £6,000.

- Over £16,000: You are not eligible for Universal Credit.

This reduction is calculated as “tariff income”, which is an assumed income generated from your savings, even if you’re not actually earning any interest.

Real-Time Example:

Sam is a single claimant with £6,300 in a savings account.

- Her capital over the £6,000 threshold is £300.

- For every £250 (or part thereof), £4.35 is deducted from her monthly Universal Credit.

- In Sam’s case, £300 is counted as two parts of £250, so £8.70 is deducted from her monthly benefit.

Similarly, Leeroy has £14,500 in savings.

- That’s £8,500 over the lower threshold.

- £4.35 is deducted for every £250 of this amount.

- £8,500 ÷ £250 = 34

- 34 x £4.35 = £147.90, deducted per month from his Universal Credit.

And if someone like Helen has £17,000 in savings, she is ineligible because her capital exceeds the £16,000 upper limit.

Universal Credit Capital Threshold Impact:

| Total Capital | Amount Over £6,000 | Monthly Deduction | Eligibility Status |

| £6,300 | £300 | £8.70 | Eligible with reduction |

| £10,000 | £4,000 | £69.60 | Eligible with reduction |

| £14,500 | £8,500 | £147.90 | Eligible with reduction |

| £16,000+ | £10,000+ | Not Applicable | Ineligible for UC |

These figures highlight the direct impact your savings have on your entitlement, making it critical to track your capital closely.

What Counts as Savings for Universal Credit?

So, what exactly qualifies as “savings” or “capital” under Universal Credit? The definition is broader than many expect. It doesn’t just mean cash in your bank; it includes a wide range of financial assets, both tangible and intangible.

Cash and Bank Accounts

All accessible funds are counted. This includes:

- Cash savings held at home

- Money in personal or joint current accounts

- Savings accounts in banks, building societies, or credit unions

- Online accounts and e-wallets like PayPal

- Help to Save or Post Office accounts

Even if the money is not currently being used, if it’s accessible to you, it is considered capital.

Investments and Lump Sums

The list of investable capital that is taken into account includes:

- Stocks and shares

- Premium Bonds

- All types of ISAs: Cash, Stocks & Shares, Help to Buy, Lifetime ISAs

- Dividends and other investment income

- Redundancy payments

- Inheritance money (whether spent or not)

- Compensation settlements

- Funds in trust accounts (unless explicitly excluded)

- Cryptocurrency assets such as Bitcoin or Ethereum

- Unspent benefits or tax rebates

Properties and Financial Interests

Any property you own, other than the one you live in, is likely to be considered capital. This includes:

- Second homes

- Holiday lets

- Land

- Buy-to-let properties

- Any property where your name appears on the title or mortgage, even if someone else lives there

If you’ve been added to someone else’s mortgage (e.g., helping a relative), the value of that interest must still be reported.

What Types of Savings and Assets Are Not Counted for Universal Credit?

Not everything you own is considered savings. Certain items are excluded by default or under specific rules, especially when they do not represent liquid or accessible assets.

Examples of excluded assets:

- Your main home

- Household contents (furniture, appliances, etc.)

- Personal possessions (e.g., jewellery, clothes, electronics)

- One vehicle (car, motorbike, etc.)

- Most pension funds (until accessed)

- Child savings in their own names (e.g., Junior ISAs, Child Trust Funds)

- Life insurance policies that have not paid out

- Funeral plans or contracts

In some cases, even money received from the sale of your home may be disregarded for up to six months, provided it’s being used to buy a new home.

Similarly, welfare support payments and certain compensation schemes are exempt from being treated as capital, either temporarily or permanently.

How Are Property and Other Assets Treated in a Universal Credit Claim?

Property can be complex when it comes to Universal Credit eligibility. The home you live in is not treated as savings. However, other properties may be considered capital depending on circumstances.

Properties You Do Not Live In

Properties that you own but don’t live in can significantly affect your entitlement. Unless covered by an exception, their full market value, minus mortgages and selling costs, is added to your capital total.

There are some exemptions, such as if the property is the main residence of:

- A close relative who is retired or disabled

- A former partner who is a lone parent

If no exemption applies, you may need to obtain a valuation to declare its value accurately.

Business and Commercial Properties

If you own a property used for a business, such as a café, guesthouse, or rental office, and the business is still operating, it is not counted as capital.

However, if the business has ceased trading for more than six months, the property may start being considered part of your capital assessment.

What Happens If You Intentionally Reduce Your Savings?

When someone attempts to lower their capital to qualify for or increase Universal Credit, this is known as deprivation of capital. Examples include:

- Gifting money to relatives or friends

- Moving large sums into a child’s account

- Making expensive but unnecessary purchases

- Transferring property to someone else’s name

If the DWP believes this was done with the intention of claiming benefits, they may treat the money or asset as if you still have it. This is called notional capital.

It may result in:

- A reduction or loss of your Universal Credit

- Repayment of overpaid benefits

- Possible penalties or legal action for fraud

It’s critical to keep full records of how savings were spent, particularly for large or irregular transactions.

How Can You Legally Reduce Your Capital for Universal Credit Purposes?

If your savings exceed £16,000, there are legitimate ways to reduce your capital that won’t be penalised, as long as they are reasonable and necessary.

These include:

- Paying off credit cards or outstanding personal loans

- Settling rent or mortgage arrears

- Making essential home repairs or adaptations (especially for health or safety)

- Purchasing a reliable vehicle for work or family needs

- Replacing worn or broken household appliances

The key is to ensure that any expenditure is proportional to your needs and not excessive. Keep receipts and documentation in case you’re asked to explain how money was used.

What Should You Do If Your Savings Increase or Decrease?

Life changes quickly, and your financial situation may shift due to:

- Receiving an inheritance

- Selling a property

- Business closure

- Investment returns

- Compensation payments

Any increase or decrease in savings must be reported immediately via your Universal Credit online account. Failure to report changes could result in overpayments that must be repaid, potentially deducted from future benefit payments.

Examples of Reportable Capital Changes:

| Scenario | Action Required |

| Received inheritance | Report as soon as funds are received |

| Sold a second property | Declare the capital and update your savings |

| Opened new investment account | Add under savings section of your UC journal |

| Business closure with remaining funds | Declare within 6 months or sooner |

Are There Any Support Options if Your Savings Disqualify You From Universal Credit?

If your capital exceeds the £16,000 limit, and you are no longer eligible for Universal Credit, you may still be able to get help through other schemes.

Alternative support options include:

- Council Tax Reduction: Often available even if you’re not on Universal Credit

- Discretionary Housing Payments: For short-term rent support via your local council

- Charitable grants: Offered by non-profits and organisations for those in hardship

- Food banks and crisis support: Emergency help if you’re unable to meet daily needs

- Financial advice services: Free assistance with budgeting, debt, or benefits planning

In many cases, if your capital later drops below £16,000, you can reapply for Universal Credit and go through a new assessment.

Conclusion

Knowing what counts as savings for Universal Credit is essential to protect your eligibility and avoid financial penalties. From bank accounts and investments to second properties and compensation, a wide range of assets are considered when determining your entitlement.

Equally, knowing which assets are exempt and how to manage changes to your capital gives you more control over your Universal Credit journey. Always report changes promptly, and if you’re ever unsure, seek expert advice.

Staying informed not only ensures you get the support you need but also helps you avoid costly mistakes and overpayments.

Frequently Asked Questions

Can I claim Universal Credit if my partner has savings but I don’t?

Yes. All household savings are counted jointly, so your partner’s capital affects your claim.

Is there any grace period when receiving a large lump sum?

Yes. For example, funds from selling a home are disregarded for up to 6 months if used to purchase a new home.

Do digital currencies like Bitcoin count towards savings?

Yes. Cryptoassets are treated as part of your capital and must be declared, regardless of volatility.

What if my savings go over £16,000 temporarily?

You will become ineligible while over the limit but can reapply once your savings fall below £16,000.

How are self-employed people’s business savings handled?

Active business capital is excluded, but if your business has closed for over six months, it may be counted.

Will my Universal Credit stop immediately if my savings increase?

Yes. Your payments stop when savings exceed the limit. If unreported, this may result in overpayment.

Can I move savings into my child’s account to stay eligible?

No. This is likely to be treated as deprivation of capital and may result in penalties.

Also Read:

- Universal Credit Savings Limit | How Much Can You Have Without Losing Benefits?

- Can I Claim Jobseeker’s Allowance If I Have Savings?

- How Much Savings Can I Have on Disability Benefits in the UK?

- Do ISAs Count as Savings for Universal Credit? | Things You Need to Know!

- Can Universal Credit Check My Savings Account? | What You Need to Know?